This Month in Real Estate

June 2010

Commentary

The housing sector continues to show signs of recovery. Together the tax credit (which expired at the end of April), the more upbeat consumer confidence, and favorable market conditions all contributed to bolstering April’s sales activity – with existing home sales increasing for the second straight month.

The housing sector continues to show signs of recovery. Together the tax credit (which expired at the end of April), the more upbeat consumer confidence, and favorable market conditions all contributed to bolstering April’s sales activity – with existing home sales increasing for the second straight month.

The return of buyer confidence with much of the home price correction believed to be over, encouraging economic developments and historically low mortgage rates, will provide the stepping stone for further market stabilization.

Meanwhile, stagnant job growth and elevated levels of foreclosure continue to be cause for concern. The government is now taking proactive steps to restructure the mortgage industry with risk-management measures seen by experts as a “huge cut in red tape” that would ultimately benefit consumers.

The Housing Market

Existing Home Sales

Existing home sales strengthened in April to 5.77 million, up 8.7% from March and 22.8%from last April. This is the tenth consecutive month of year-over-year increases.

According to Lawrence Yun, NAR chief economist, although part of the uptick was expected from the tax credit, there’s also been a return of buyer confidence, for those who remained on the sideline last year. The return of confidence is a result of stabilized prices, an improved economy, and continued advantageous interest rates.

In March, 49% of sales were from first-time buyers.

Median Home Price

The median price for an existing home was $173,100 in April, up 2.1% from a year ago and 4% from March. Distressed homes, accounting for a third of last month’s sales, continued skewing prices downward slightly as they typically are discounted 15% compared to typical home sales. Overall, prices this past year showed increased stability over the previous year.

Inventory

Total housing inventory rose slightly to 4.04 million in March, representing slightly less than an eight-and-a-half month supply of sales (if homes continue to sell at the current pace consistently and no new homes come on the market). Compared to the previous year, there are now 3% more homes on the market. Although this is the first rise in twenty consecutive months of decline when compared to the previous year, NAR’s chief economist believes this increase can be attributed to the summer selling season and that home prices are back on track.

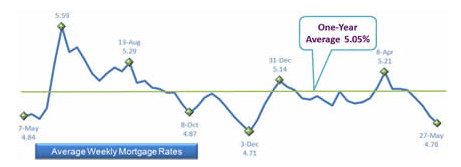

Mortgage Rates

Mortgage rates dipped back below 5% this month due largely in part to the European debt crisis. As confidence in the value of the Euro eroded, more investors chose the U.S. dollar instead. With more demand for dollars, the cost of debt (interest rate) dropped. This event has also shown the global recovery is not free-and-clear of roadblocks to complete recovery. However, experts still anticipate rates will increase to between 6% and 6.5% by the end of the year. As the recovery gains increasing traction, the Federal Reserve will need to increase rates to prevent inflation.

Affordability

Affordability remains advantageous, supported by some of the lowest mortgage rates in decades as well as less expensive home prices. The home price-to-income ratio continues to remain well below the historical average of 25%. The ratio now stands at 14.9%.

Sources: National Association of Realtors, Freddie Mac

Government Action

FHA Turns to Lenders to Monitor Brokers

As the Federal Housing Administration (FHA), the government agency that insures home loans, saw its market share rise to about one-third of the mortgage market last year, up from 2% in 2006, the number of brokers seeking to arrange FHA-backed loans has mushroomed to 9,043 at the end of 2009 from 5,759 just two years earlier.

As the Federal Housing Administration (FHA), the government agency that insures home loans, saw its market share rise to about one-third of the mortgage market last year, up from 2% in 2006, the number of brokers seeking to arrange FHA-backed loans has mushroomed to 9,043 at the end of 2009 from 5,759 just two years earlier.

The agency, finding itself inadequately equipped to monitor its brokers, is shifting the responsibility to its lenders.

The FHA expects the new policies to result in better risk management, and the cut in red tape should produce better rates for consumers.

As of May 20, the FHA no longer certifies mortgage brokers or tracks the performance of brokers’ loans. Instead, lenders are now required to sponsor brokers and assume responsibility for loans they originate, including losses from fraud or mistakes in underwriting. In addition to revamping broker insight, the agency also beefed up oversight of its lenders by increasing net-worth requirements to $1 million from $250,000. The change is in effect for one year for existing lenders.

Source: WSJ.com

Topics For Buyers and Sellers

Myths about Distressed Properties – Debunked!

Distressed properties – foreclosures and short sales alike – represent potentially great value for prospective buyers. However, common misconceptions about the time and money investment involved with buying such properties may keep many from inquiring further into this market. Keller Williams Research survey findings, taken from more than 2,500 Keller Williams associate respondents who have worked with distressed properties, can help steer clear of concerns as you make your way to homeownership.

Brought to you by Keller Williams Research.

Please “Contact Me” if you have Real Estate interests in Sarasota and the Bradenton Florida area.